Velera Payments Index: Consumer Spending Remains Strong Despite Rising Gas Prices

- Roy Urrico

- Apr 22

- 5 min read

By Roy Urrico

“Despite skyrocketing gas prices since the start of the war with Iran, spending remained robust in the goods, services and money services sectors, fueled in part by higher income tax returns and some temporary relief from TSA bottlenecks during the partial government shutdown.” These are among the findings from the April edition of the Velera Payments Index, which also included a quarterly metrics update, along with closer looks at gasoline consumption, balance transfer behavior and credit card balances.

St. Petersburg, Fla.-based Velera, which describes itself as the nation’s premier payments CUSO, produces the Velera Payments Index to help credit unions and other financial institutions make strategic, data-informed decisions.

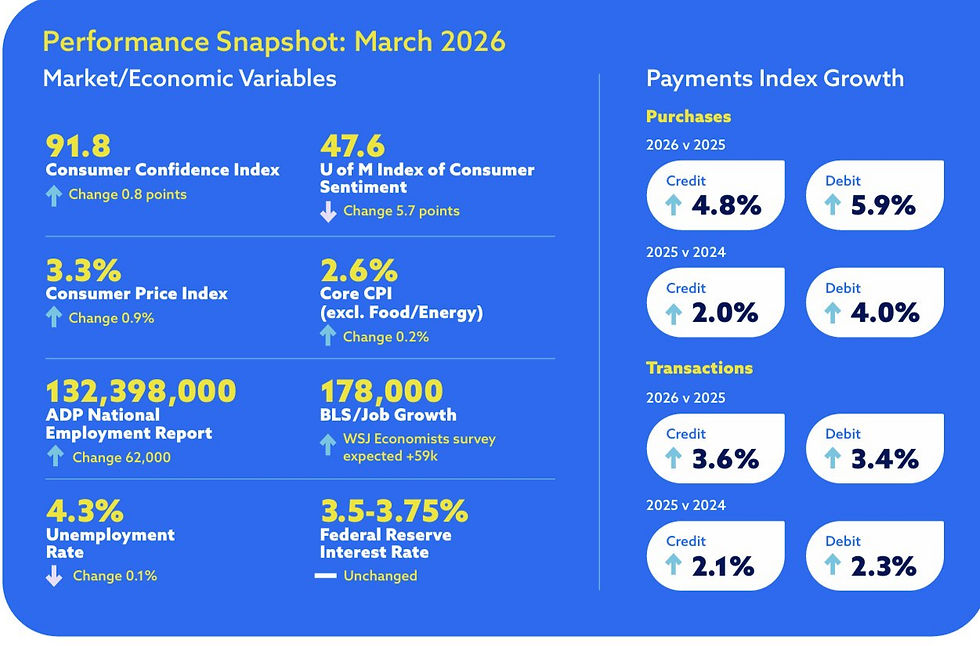

Some Economic Indicators

From the Velera Payments Index:

Year-over-year growth in transactions and purchases for March remained strong for both debit and credit. Debit purchases increased by 5.9%, with the money services and goods sectors accounting for almost two-thirds of that growth. Credit purchases were up 4.8%, with the goods and the service sectors accounting for 63% of the increase. In March, debit transactions were up 3.4% and credit transactions rose by 3.6%.

For March, the Bureau of Labor Statistics (BLS) reported a 0.9% increase in inflation, increasing the 12-month Consumer Price Index (CPI) to 3.3%. The Energy Index was the largest contributor to the monthly increase, up 10.9%. Gasoline accounted for nearly 75% of the overall energy increase. Core CPI, which excludes food and energy, rose 0.2% in March, finishing the month at 2.6%. Categories contributing to the Core CPI increase included airline fares, apparel, household furnishings and operations, education and new vehicles. March also saw declines in medical care, personal care and used cars and trucks.

In its preliminary April 2026 results, the University of Michigan Index of Consumer Sentiment dropped 11% from March (56.6), posting a 5.7-point loss to 47.6. All demographics (age, income and political party) posted declines in sentiment.

For March, the Conference Board reported that consumer sentiment inched higher in the Consumer Confidence Index, up 0.8 points to 91.8. While there was a modest improvement in three of the five components of the index, the overall score has declined since 2021.

The BLS reported jobs grew by 178,000 positions in March. The unemployment rate ticked down to 4.3%, or 7.2 million people. March job gains were primarily in healthcare and construction, as well as transportation and warehousing, while job losses in the federal government continued for the month. The March ADP jobs report, which tracks changes in U.S. private employment, reported an increase of 62,000 jobs, mostly centered on the education and health services, construction and information sectors. Job reductions were noted in the trade, transportation and utilities, and manufacturing sectors.

The U.S. Gross Domestic Product (GDP) for the fourth quarter of 2025 was revised to 0.5%. Consumer spending accounts for just over two-thirds of GDP and was revised downward to 1.9% from 2%.

In March 2026, digital wallets accounted for 12.6% of all debit transactions, up from 10.2% a year earlier, and 7.3% of all credit transactions, up from 5.6% a year earlier.

“Consumers are still showing up and spending, even with many factors weighing on how they feel about the economy,” said Denise Stevens, EVP, chief product and technology officer, Velera. “Surging gas prices, elevated inflation and overall uncertainty have not stopped spending activity – but they are changing behavior. We’re seeing consumers be more intentional about how they pay and spend, including continued notable growth in digital wallets. At the same time, buy now, pay later has gone mainstream as a budgeting tool, not just a checkout convenience.”

Other Key Takeaways

Gasoline consumption: At the time of the Velera publication, the average price in the U.S. for a gallon of gasoline was $4.12, up $1.19 or 40% since the end of February 2026. “While the prices are up, our check-in this month is focused on consumer demand. Have consumers changed their behavior due to higher gasoline prices?” Velera asked. Its data shows the opposite. “We see that the indexed weekly volume of gasoline purchased at automated fuel dispensers (AFDs) has been higher since the start of the war in late February for both debit and credit card purchases.”

For March, monthly gasoline sector purchases were up 14.1% on debit and 18.1% on credit. Gasoline transactions were up 5% on debit and 5.2% on credit when compared to March 2024. “In summary, with higher gasoline prices, consumers appear to be purchasing more gallons and making more transactions than in March 2025, at least in the short term,” said the Velera report.

Balance transfers: “The first quarter of each year remains the peak month for balance transfer/ convenience check usage. Whether used to pay off high-interest rate credit cards from holiday spending or to pay taxes owed, they remain a useful and appreciated tool for members,” noted the Index. “We consistently see an annual cycle with elevated activity in the first three months of each year, but in 2025, there was also an uptick in monthly transferred dollars from August through the end of the year.” Year-over-year, the number of balance consolidation transactions was flat at 0% when compared to March 2025. For those who used balance transfers in March 2026, the average balance transfer amount was $4,917, up $6 compared to 2025.

Credit card balances: Card balances have softened during the first quarter of 2026, trailing the same period in 2025. In March, the average balance among gross active accounts was $2,930, down 0.7% (or $21) from a year earlier. Total credit card balance growth was also negative, declining 1.5% year-over-year. “This moderation reflects not only typical holiday spending paydown, but also a meaningful shift in consumer cash flow,” said Velera. Credit card delinquencies during the first quarter of 2026, the credit card delinquency rate followed the typical pattern of gradual improvement after peaking in January. In March, the delinquency rate stood at 2.49%, up 18 basis points (or 7.8%) from a year earlier and 16 basis points lower than the January level of 2.73%.

What Credit Unions Should Do Now

The Index recommended opportunities for credit unions such as:

Boost top-of-wallet behavior with strategic awareness campaigns. “Awareness campaigns are a cost-effective way to keep your card top of mind without relying on incentives. By highlighting your financial institution's benefits and core card features, you reinforce everyday relevance and strengthen top-of wallet behavior,” the report stated.

Elevate member engagement through proactive, personalized interactions. Velera suggested: “Payments are among the most frequent touchpoints members have with their credit union, making engagement a powerful driver of loyalty. Proactive, personalized interactions – such as financial education and wellness guidance, loyalty-building rewards and promotion of digital banking capabilities – strengthen member connections and long-term value.”

Drive seasonal payment growth with targeted, data-driven engagement. “Targeted engagement is essential to a strong payments strategy. Using data driven insights to deliver timely, seasonal campaigns helps credit unions boost payment activity, deepen relationships and deliver meaningful value. Usage campaigns efficiently influence cardholder behavior during high spend periods like back-to-school.”